You may be wondering, “Why should I even plan? What's the whole point?” This is a great place to start.

According to the American Psychiatric Association, over 70% of adults worry about money. This results in stress, prolonged exposure to which can lead to physical ailments such as heart disease, migraine headaches, and poor sleep.

If worrying about money causes stress, then would the opposite not also be true? Not having to worry about money frees you up to do other things with your mental and physical energy, not to mention that eliminating financial stress will hopefully add years to your life, rather than subtract from it. Also, you should know that the number two reason for divorce is money (the number one reason is infidelity). Having a plan for your finances can also save your marriage.

In the Wizard of Oz, the yellow brick road leads to Oz. Think about retirement planning as though you’re creating your own yellow brick road, your own path to success. That’s what a retirement plan is designed to do. It’s taking everything we know right now about your life: your goals, hopes and dreams but also the risks you face, the income you generate and all the other realities of your financial picture. You take all these data points and with the help of a knowledgeable guide, and an experienced financial advisor, put together a step-by-step path to getting to your destination. Obviously, as time goes by, things will change. Your plan will need to be adjusted accordingly so that despite all the twists and turns, you still continue in the right direction.

Having a destination and a roadmap, even if it’s a changing roadmap, truly increases your probability of success. We know from experience that no one ever reaches their destination in a straight line, but we also know that most people who try to “wing it” rarely, if ever, reach their destination.

When people think about financial planning, their mind often goes straight to retirement. While retirement is a centerpiece of a financial plan for most clients, it’s not its exclusive focus. The good thing about having a retirement plan is that you can factor the rest of your life around it. I’ll give you a real example from my own life. My wife and I wanted to buy a vacation home, but we had to think about how this investment would affect our lives, not only over the next few years, but for some time to come. We have kids we want to put through school. We have retirement plans for ourselves. We also want to travel as a family. The first thing we did as we considered this potential second home was to plug it into our plan to see how this new commitment might affect our financial future.

If you are one of those people who gets their financial education from the media (first of all, we hope you don’t, but if you do…), you may be familiar with their focus on two questions: “When can you retire?” and “How much do you need?” Retirement planning is about scenario planning with real-life decisions. It allows you to think through how financial decisions today may affect your financial future, whatever your goals may be. Our clients come to us with all kinds of questions about their retirement plans, questions that at first glance have nothing to do with retirement. Unexamined, these decisions they are weighing will have an impact on their retirement plans, too, of course. People ask us about buying second homes or boats, about being able to afford their kids’ college tuition, and sometimes they may even ask if we think they can afford to have a third, fourth, or fifth child! How would that impact your retirement?

The trouble with the terms “financial planning” and “retirement planning” is that they are inaccessible to most people. We wish there were a more exciting way to name this critical exercise of looking at all the amazing things you want to do with your life, and figuring out a plan to make them happen! Some people are turned off by the idea of planning, because they think they aren’t old enough, don’t have enough money, or it’s so far down the road, they don’t think they need it. What we want to scream at the top of our lungs is that retirement planning is not just as you approach retirement. The younger you are when you start doing this, the more successful you will be in getting to your goal. The chances of you making better financial decisions increase dramatically the sooner you engage in this process. Maybe they should call it “success planning.”

This is the question everyone wants answered. As a financial advisor, I am obligated to ask you a question in return. That question is, “What kind of retirement do you want?” And by that, I mean, how do you want to live in your retirement? I keep on seeing articles about people who claim they retired at age 40 with a million in the bank. All I can think of is, that’s great, but how in the world are they going to live off forty thousand dollars a year (the approximate amount of income they can conservatively produce from their savings without touching their principal). Plus, they must get insurance, and things keep costing more every year, and, and, and…

I don’t know about you, but that’s not the lifestyle I want. In any event, the question is, “what is the lifestyle YOU want?” Usually, you’ll look at the lifestyle you are leading now, since we know (or can quickly figure out) how much that’s costing. Do you want to continue your current lifestyle, or change it in any way? How much money will you want to spend on an annual basis? Will you want to travel? Will you want to contribute to a cause or charitable organization? You really need to have a sense of how you will want to spend your retirement.

Now you will need to tell me how soon you want to be living this way. Any capable financial planner will be able to tell you how much money you’ll need the moment you retire, and how much you’ll need to save over how many years to get there. From that standpoint, it’s simple. Math is not the difficult part. The hard part is figuring out how you want to live. If you are already saving, or have some money in the bank, that too, is factored into the calculation. And of course, there’s always the issue of not knowing how long you will live, so we must make some assumptions there, too.

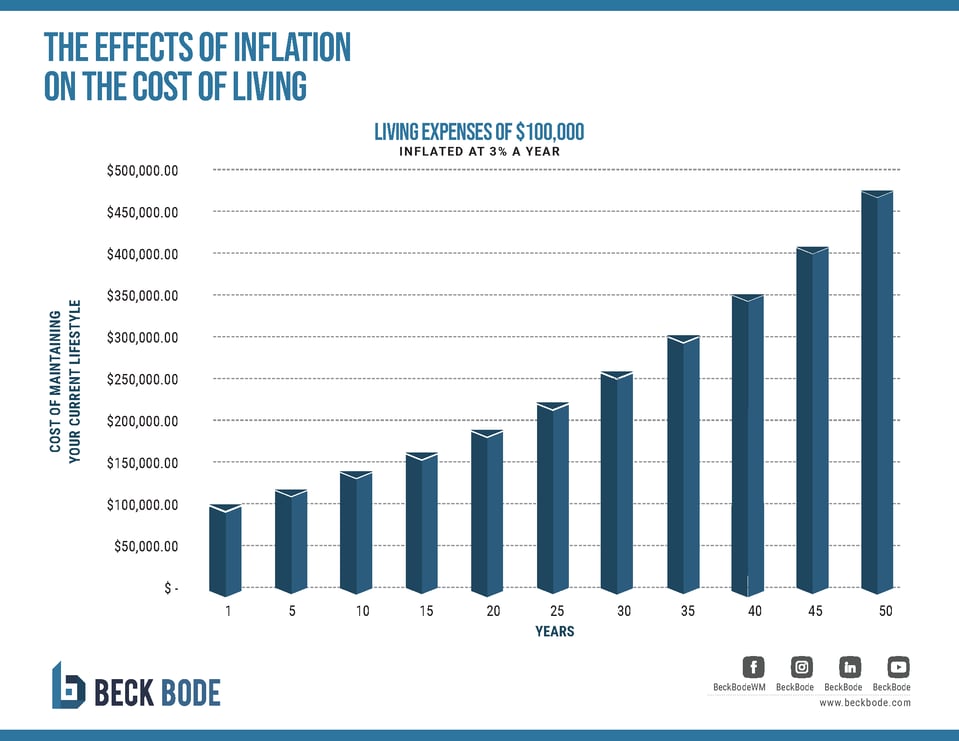

Every financial plan has living expenses going up at a certain percentage, typically around 3% a year. That’s an assumption that can be adjusted in whatever software it is that is used for modeling your scenario. Let’s just assume your annual living expenses today come to $100,000. If expenses were to increase at 3% a year, for the next 30 years, do you have any idea how much it would cost to live your lifestyle? It’s a mindboggling $250,000 (approximately). Wow!

Inflation

One of the biggest things that people disregard, or don’t take seriously when they are planning for retirement is inflation. You must factor in inflation; it is the silent killer of all financial plans. Inflation is a reality because we all know things increase in price over time. A solid retirement plan has to face those rising costs, especially because the average retiree, provided they’re in decent health, could be in retirement for three decades or more! That’s thirty years that your investments need to keep up with ongoing inflation, not to mention your committed financial needs. Your investment portfolio needs to be specifically designed to outpace inflation so that you can avoid the disaster of eroding buying power over time.

Lastly, a solid retirement plan must be built to withstand surprises that are simply a part of life. How you handle the curveballs that life throws you dictates how they will affect your financial future. The things that could affect your plan could be a change in income (either through the loss of a job, or perhaps an increase in revenue). Other financial changes could be death, long-term illness or the need for long-term care, divorce, the birth of a child. All these things have a potential financial impact. One of the most frequent questions we get is when people want to leave their current job, and they want to know what the lowest amount of income is they need to generate without jeopardizing their retirement.

We can use financial planning software to model these scenarios and provide answers that can help with our clients’ decision-making.